Choppy markets see stocks flat and crude retrace gains

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Wall Street ends narrowly mixed on a volatile trading day

* USD surges on haven status on energy independence, EUR suffers

* President Trump won’t rule out sending US troops into Iran ‘if necessary’

* US natural gas jumps alongside global gas, oil prices

FX: USD broke out to the upside after the recent consolidation below the 50-day SMA, that now sits at 97.90. The strong move pushed above the 200-day SMA at 98.35. The US is far more energy-independent than Europe and much of Asia. When oil and gas prices jump, energy-importing economies see their trade balances worsen, which can pressure currencies like the euro and yen. We saw this in 2022 when sustained high oil prices above $100 helped drive a strong dollar trend. If energy stays elevated, this dynamic may return, as well as push Fed rate cut bets further out if price pressures remain persistent or even rise.

EUR broke down below its 50-day SMA at 1.1775 and got close to the 200-day SMA at 1.1662. As per above, net importers of oil suffer in the current environment. The announcement that Qatar Energy had halted LNG production also hit the single currency hard. Investors may re-appraise their view of a resurgence in European industry, though the global economy is in a much better position than it was when energy prices spiked in March 2022, with more fiscal support. The year-to-date low is 1.1576.

GBP outperformed all its peers apart from CAD and AUD. There could be a material improvement in the UK’s fiscal picture as we head into today’s Spring Statement update. Stronger than expected cash tax receipts are driving expectations for a decent reduction in UK bond sales. Cable dipped to a major Fib level at 1.3338 before closing marginally lower on the day and well off its lows.

JPY underperformed as the major pushed off the 50-day SMA at 156.02. The normal safe haven characteristics of the yen were shattered by surging energy prices, as we highlighted above. Prices are nearing the early February election levels at 157.66, next stop would be the intervention barrier around 159. Domestic comments from a BoJ official offered little guidance on the policy outlook ahead of the next BoJ meeting on March 19.

CAD and AUD outperformed, albeit with losses versus the dollar, supported by soaring oil and metals prices.

US stocks: The S&P 500 added 0.04% to close at 6,881, the Nasdaq was 0.13% higher at 24,992 and the Dow Jones settled lower by 0.15% at 48,904. Four sectors led the gains with Energy, Industrials and Tech strongly outperforming. Consumer Staples, Consumer Discretionary and Healthcare were the biggest laggards. The S&P 500 found support at the 100-day SMA at 6,833. Defensives in the Dow didn’t save it from settling in the red, as buyers bargain hunted beaten up tech and software stocks. Defence companies like RTX and drone maker KTOS surged along with oil giants like Exxon and Chevron. Inevitably, airliners, cruise liners and lodging all suffered with disruption at Middle Eastern airports including at Dubai, the busiest airport hub in the world.

Asian stocks: Futures are mixed. APAC stocks were lower on the US-Iran conflict. The ASX 200 was rangebound with strong energy offset by soft tech, financials and airlines. The Nikkei 225 slid below 58,000 as exporters suffered from the deteriorating geopolitical environment. The Hang Seng and Shanghai Comp were mixed with Hong Kong weighed down by tech again while the mainland steadied ahead of the annual “two sessions”.

Gold was up on the day came off its intraday top at 5,419 through the US session as stock markets rebounded. Bullion should be underpinned by various drivers in the current climate.

Day Ahead – Middle East

As always with any geopolitical escalations, the key question is what are the potential macro effects? In a global context, Iran and several neighbouring countries are not major macro powers, as their direct weight in financial markets is limited. This is a large part of the reason why market reaction has so far been relatively contained. We have seen in other conflicts like in Ukraine that markets quickly narrow their focus to any impact on macro transmission channels. As long as oil and gas continue to flow through the Strait of Hormuz, global markets can function even amid significant regional instability. That means the negative macro and inflationary impact is likely to be limited and looked through by policymakers. Of course, a protracted conflict is a different matter.

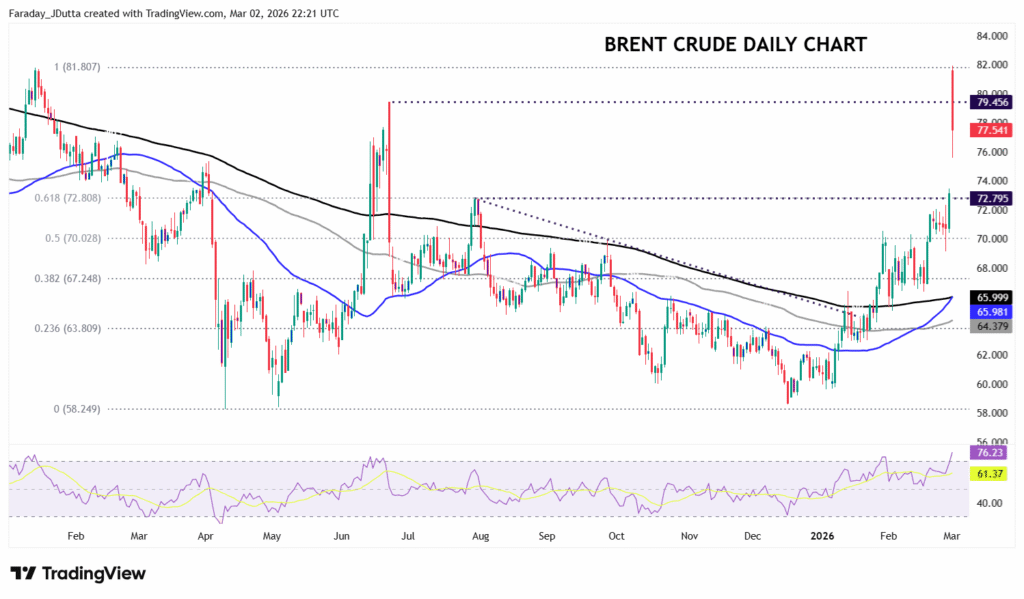

Chart of the Day – Brent hits resistance

Brent crude jumped up 13% in Asian hours before paring gains through the day and settling up around 6%. Just for context, even though it’s a big move, to get into the top 20, 10 and 5 biggest daily gains, crude would need to be up +9.6%, +13.6% and +13.9% respectively. The energy complex has been supported by the closure of the Strait of Hormuz and came after at least three ships were attacked near it at the weekend. Iran warned vessels not to pass through the crucial waterway, through which about 20% of the world’s oil and gas is shipped.

Much depends on this area and if we see a material and lasting disruption to physical oil flows. Historically, even during prior conflicts in the region including the so-called Tanker War, there has not been a full and sustained shutdown of the strait. There is also a credible path to securing tanker traffic with military assistance to ensure continued transit. Chart wise, notably Brent tapped the January 2025 top at $81.80 but then retraced back down through the June 2025 high at $79.45. The breakout level below resides just below $73.