Sentiment weighed by war, in volatile trade

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* US ponders military support for Mideast oil and gas supplies

* Dollar hits highest since January, boosted by oil independence

* Gold slumps as strong dollar, yields offset war risk premium

* Wall Street pares sharp losses though conflict fans inflation fears

FX: USD pushed up to an intraday top at 99.68 before falling after the US open and consolidating in the last few hours of trading. Prices still settled above the downward trendline from the late November high but gave back more or less half of its gains. This tallies with bond markets where yields on the 10-year Treasury pooped up to 4.11% before closing at 4.06%. Haven demand amid rising oil prices has boosted the greenback, with the US now a net exporter of petroleum. Geopolitical headlines dominated news wires making for some headline havoc.

EUR broke down below its 200-day SMA at 1.1665 though closed off its intraday low at 1.1530 and above the year-to-date low at 1.1576. As we have said this week, net importers of oil suffer in the current environment but an intraday pullback in crude was significant for the euro. That said, ECB rate expectations are up materially with December now priced for 15bps of rate hikes. If energy prices continue to ease, policy tightening could get reined in. The euro area’s preliminary CPI figures revealed a stronger than expected 1.9% y/y print with core also surprising to the upside at 2.4% y/y.

GBP fell further through the major Fib level at 1.3338 before settling above it. The intraday low in cable was 1.3253 which is now a key level for the week. The pound is second best among its peers this week, which is in line with its historical pattern of relative strength against higher-beta, growth sensitive majors. The Spring fiscal statement was pretty much a non-event, just as the Chancellor would have wanted. The OBR lowered its 2026 GDP forecast to 1.1% from 1.4% but raised 2027 and 2028 to 1.6% for both years.

JPY outperformed all its peers apart from CAD. This likely reflects some lingering haven-related strength despite the recent shift in the currency’s relationship to risk more broadly, while oil prices gave back around half of their day’s gains which also helped. We also got some verbal intervention from a MoF official who said the government was ‘monitoring’ markets with ‘utmost vigilance’.

US stocks: The S&P 500 lost 0.94% to close at 6,817, the Nasdaq was 1.09% lower at 24,720 and the Dow Jones settled lower by 0.83% at 48,501. The benchmark S&P opened down and was off close to 2.5% on its lows before bouncing back through the session. A bullish hammer candle printed where the closing price is much greater than the opening price, indicating that buyers had control of the market before the end of the trading period. The same pattern printed on the Dow Jones as well. Every sector was in the red with materials and industrials the biggest laggards. Financials and Communication Services were the outperformers, albeit still negative on the day. Target was the big winner as it jumped 6.7% on a strong 2026 outlook despite a sales slump. Interestingly the battered software sector rose for a second straight day while defence stocks like Northrop Grumman, RTX and Kratos gave up some of Monday’s gains. Cruise liners and airliners slid again extending heavy selling this week though they broadly closed off their lows.

Asian stocks: Futures are mixed. APAC stocks followed global stocks lower as the Middle East conflict entered into a fourth day. The ASX 200 declined led by mining and materials with broad weakness. The Nikkei 225 fell below 57,000 while jobless data stoked inflationary worries. The Hang Seng and Shanghai Comp eventually succumbed to the downbeat mood with investors awaiting the Two Sessions.

Gold was choppy as it dipped below $5000 after the US open before rebounding through the session. That psychological level is also the midpoint of the late January to early February move. But the bounce back didn’t take bullion back above the 61.8% major Fib level at $5,141. While many expected gold to hold a safe haven bid, the sell-off especially in silver shows the crowded nature of positioning going into this volatility, with some dollar strength, profit taking, and liquidation seen more broadly in precious metals. When the top trending stocks on sites like Wallstreetbets are gold and silver, that’s not good for bugs.

Day Ahead – Middle East

Oil and natural gas remain the biggest drivers of markets at present. For what it’s worth, we are also following Flight Radar24 and marine traffic, having got up to speed with missile maths and interceptors. The latter still points to a shorter conflict than a major war. While the market started to de-risk yesterday, oil again bumped into resistance at the 2025 high, which is proving stubborn to close above. Elevated crude does raise the question as to what point does potential inflation pressure from higher prices dominate rates, versus the negative impact from weaker growth prospects which pulls bond yields lower. But we still think a sharp spike may be looked through by policymakers. Interestingly, crude and the dollar were off their best levels as US President Trump announced measures to ease the impact of the war on the economy. He also said the US will offer political risk insurance and guarantees for financial security of all maritime trade, especially energy, travelling through the Gulf with US Navy exports to tankers if needed. The flow of oil and gas is critical for global markets and any monetary policy impact.

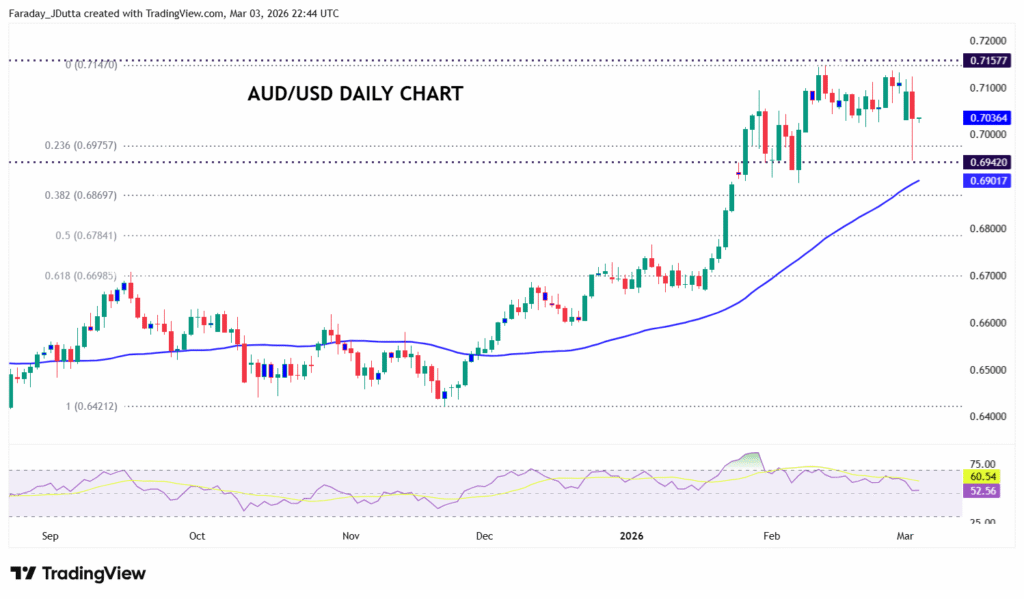

Chart of the Day – AUDUSD bounces off support

Chart wise, the aussie recently pulled back from multi-year highs, having hit resistance at the January 2023 top at 0.7157. Prices were overbought after six straight weeks of buying and retraced into a range and then yesterday fell to the October 2024 top at 0.6942. There’s a minor Fib level at 0.6975 but prices are back in the range after bouncing hard, with rising aluminium prices especially supporting AUD. It’s noteworthy that it’s a cyclical currency has outperformed some of its peers like NZD in this hugely volatile week.

Domestically, RBA Governor Michell Bullock warned on Monday that the March meeting is a live meeting as the RBA board will “be actively looking whether or not it needs to move more quickly”. In fact, she explicitly questioned the market assumption that the RBA will mostly likely wait for quarterly inflation data to adjust policy. The comments come as monthly January inflation at 3.8% y/y surprised on the high side and stayed well above the 2-3% RBA target band. At the same time, labour market data remained solid with the unemployment rate easing to 4.1%. Today’s Q4 GDP figures (0.8% q/q expected) will give additional data for the upcoming meeting. Money markets raised bets on a March rate hike from 15% to 30%.