Risk-off to risk-on, but not all-in

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Trump says negotiating with Iran, IRGC outlets deny talks

* Oil tumbles after Trump puts hold on US strikes for five days

* Dollar ditches gains as GBP stays bid above 1.34

* Stocks jump as Trump uses ‘escalate to de-escalate’ tactics

FX: USD endured a wild day along with all financial markets, after President Trump’s Truth Social post. The greenback had been rising on increased tensions over the weekend, but this was upended with Trump’s ‘productive’ talks with Iran and a 5-day postponement of strikes on their power plants. Oil prices tumbled, and with them Treasury yields. A 15% chance of a December Fed rate hike was cut back to less than 5%. The 2-year yield had spiked above 4% earlier in the day before retracing back to 3.85%. There are lots of Fed speakers this week to make sense of the current environment.

EUR rose after the POTUS post and hit an intraday high at 1.1639 before closing just above 1.16. Sentiment dominated across halves of the day though there was some scepticism over the durability of any ceasefire. Some think the Iranian price for peace, and the reopening of the Strait of Hormuz, is likely to be something which the US will struggle to accept. ECB President Christine Lagarde is due to deliver remarks on Wednesday and there are plenty of other speakers to watch.

GBP outperformed most of its peers as gilt yields, which had risen the sharpest, pulled back. Around 100bps of hikes for 2026 was cut back to 62bps through the day. We hear from Chief Economist Pill today, and from other MPC officials Greene, Breeden and Taylor later this week. Rate expectations may be sensitive to any remarks. CPI data is published on Wednesday but is rather stale. Cable is trying to get above the 200-day SMA at 1.3431 and the 50% marker of the November to January move at 1.3439.

JPY strengthened on Trump’s comments as the major backed off the strong resistance zone around 159.50/160. That was probably the line in the sand for FX interventions before the Iran conflict, but there is an obvious disincentive to intervene in a volatile market. That said, we did get comments from a MoF official who re-iterated the government’s threats of FX market intervention.

US stocks: The S&P 500 added 1.15% to close at 6,581, the Nasdaq was 1.22% higher at 24,189 and the Dow Jones settled higher by 1.38% at 46,208. All three main indices touched their 200-day SMAs but closed below them. Major fib levels (38.2%) of the May 2025 low to record high sit at 6,530 and 24,054 on the S&P 500 and Nasdaq. All sectors were in the green with cyclicals doing well with Consumer Discretionary by far the biggest winning sector, and Materials, Tech and Industrials the next best. The VIX, Wall Street’s fear gauge retreated from an intraday spike above 31, back to 26. The March high sits just above 35. There’s roughly a 13% chance of a December Fed rate hike, down from 25% at the start of the week. Banks and airlines rallied with the latter highly sensitive to jet fuel prices which had risen +240% since the Iran conflict began.

Asian stocks: Futures are mixed. APAC stocks dropped sharply on the ratcheting up in tensions between President Trump and Iran. The ASX 200 retreated with miners, materials and resources underperforming. The Nikkei 225 slumped below 52,000 and intraday losses of over 2,000 points on return from a 3-day weekend. Energy headwinds are a big drag on stocks. The Hang Seng and Shanghai Composite moved lower on the muted regional mood.

Gold whipsawed on the conflicting headlines – see below for more.

Day Ahead – Global PMIs

Flash business activity data for March released today will give a first reading of how the war has hit corporate sentiment as markets fear the risk of stagflation has grown. Most of the impact of higher energy costs, both direct and indirect, has yet to be felt, but PMI survey numbers will provide an early impression and offer a comparison between the impact on different parts of the world. Asia and Europe are considered much more exposed to higher energy costs than the US, though the effects will be global. Business activity picked up in most economies in February and the danger is the war has caused a significant reversal.

Services activity is still resilient and in expansionary territory. Manufacturing has enjoyed a decent start to the year, with notably the eurozone printing above 50 at a 44-month high. Input costs will be watched as they were high and rising into the conflict.

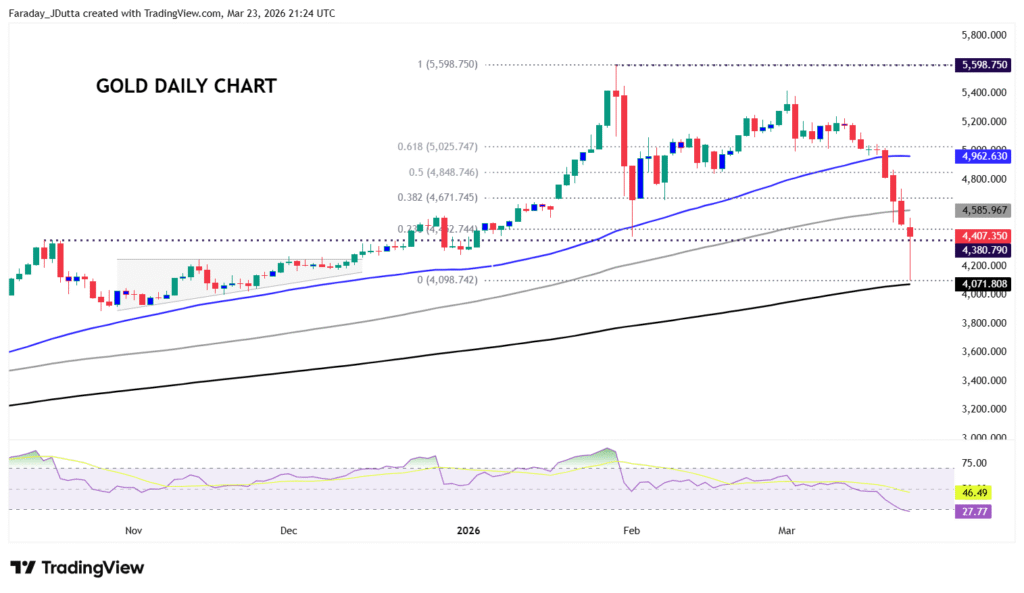

Chart of the Day – Gold plunge retraces

Bullionplunged early on Monday to kick off the week, as the liquidity needs of investors outweighed safe haven demand. There is an old market adage, “sell what you can, not what you want”. A stronger greenback and gold’s high liquidity make it a source of funds during stress episodes. This pattern is consistent with previous shock episodes, where needs for cash tend to outweigh safe-haven demand in the early stages. Macro has also been trumping bullion’s traditional strength, as rising real yields, dollar and inflation expectations have impacted short-term demand. More broadly, geopolitics alone rarely drives gold prices in a sustained way; more important is how shocks like we are seeing feed through to inflation, monetary policy and the dollar.

Prices have fallen for nine straight days, that was last seen in October 2023. Gold plunged double digits percentage in early trade close to the 200-day SMA at $4,071. But a big retracement took place post-Trump’s Truth Social post mid-morning in the European session. Gold is back at the October highs and February spike low around $4,400/4,380. The 100-day SMA sits above at $4,585. The first minor Fib retracement level from yesterday’s spike sits at $4,453.