Weak month ends with “risk on” on de-escalation hopes

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Iran President says has ‘necessary will’ to end war, seeks guarantees

* Trump tells NY Post war against Iran won’t last ‘much longer’

* Crude, USD, Treasury yields decline as more positive mood lifts markets

* Wall Street rallies as traders bet on potential war off-ramp

FX: USD made a fresh cycle high but the strong resistance zone at recent and November highs around 100.34/54 did its job. That saw the greenback reverse and slide back below 100. The risk-on environment was essentially down to Iran’s President stating that the country is ready to end the war, if provided with guarantees against future attacks. This gave some validation that the US is actually speaking to Iranian officials and that there is some progress towards an end to military action. Increasingly, it looks like the April 6 deadline that Trump set might actually work. Some month-end fixing may be at play with dollar selling coming through as the buy-side rebalances its portfolios after US stocks modestly outperformed overseas stocks. Fed Chair Powell didn’t add any fuel to the view of early Fed hikes yesterday, so that also helped at the margin.

EUR outperformed its peers as the risk mood shifted on lower energy prices. March inflation rose 2.5%, up from 1.9% in February but in line with estimates. Core inflation rose 2.3%, below forecasts and a little below the prior 2.4% print. Soft core and services data give policymakers some breathing room as they assess the impact of rising energy prices. The November low sits at 1.1468, with the mid-March low at 1.1410.

GBP was mid pack among other major currencies. Final Q4 GDP data rose 0.1%. A minor fib level of the November to January move resides at 1.3193 and below here is November low at 1.3010.

JPY strengthened again with the major falling back to the January 2025 and mid-January 2026 highs. US Treasury yields fell for a third straight day with the 2-year, which correlates strongly with the Fed Funds rate, moving below 3.8% having hit 4% on Friday. Softer Tokyo inflation didn’t deter yen strength, with an April BoJ rate hike still in play due to elevated oil prices and rising Shunto wage growth.

US stocks: The S&P 500 jumped 2.92% to close at 6,529, the Nasdaq was 3.43% higher at 23,740 and the Dow Jones settled higher by 2.49% at 46,341. Wall Street enjoyed its best day since May on the potential Middle Ease de-escalation. That said, the relief rally failed to erase volatile March with a 5.3% drop in the S&P 500 representing its worst monthly performance since 2022. Communication Services topped the leading sectors, up 4.41%, with Technology rising 4.24%, Consumer Discretionary up 3.27% and Industrials up 3.23%. The only sectors in the red were Energy and Utilities. Nvidia partnered with Marvell on AI infrastructure and silicon photonics with NVDA investing $2bln in MRVL. NVDA jumped 5.6%, Marvel soared 12.8%. Meta gained 6.7% after it said it was adding Instagram Plus and $499 Ray-Ban glasses. Nike reported profit declines after the close as weak demand in China dragged on. The stock was down 3%.

Asian stocks: Futures are mixed. APAC stocks were lower as the Houthis, the Yemen rebel group, entered the conflict by firing missiles towards Israel. The ASX 200 saw tech and financials lead the downside with energy and commodity sectors offsetting losses. The Nikkei 225 was pressured by higher oil prices and hawkish BoJ minutes. The Hang Seng and Shanghai Composite were mixed with BYD and bank earnings, and trade tensions evident.

Gold rose for a third straight day which hasn’t been seen since early March. The 3.4% jump was the best day since early February. Prices beat the 100-day SMA at $4,617. Falling Treasury yields again gave bugs some respite. So too yesterday’s comments from Fed Chair Powell and Williams who indicated policy remains in a good place, helping to temper rate-hike expectations.

Day Ahead – US Retail Sales and ISM Manufacturing

Consensus expect headline US retail sales to rise 0.4% and ex autos 0.3%. Solid gains should be driven by higher vehicle sales and a jump in gasoline prices. Going forward, the risk is that continued higher energy prices are demand destructive and hurt consumer activity. The ‘K-shape’ in spending between higher and lower-income households narrowed slightly, but remained pronounced, reflecting ongoing divergence in wage growth. Larger tax refunds for higher-income households support spending.

ISM March manufacturing activity is expected to remain stable at 52.3 signalling moderate growth. Regional surveys have been mixed though interestingly; European manufacturing surveys have started to outperform services with notably stronger order books. As a guide, recent PMI data saw input costs rise sharply on higher energy prices, and goods selling prices increased at the fastest pace since last August. On the flip side, employment growth slowed to its weakest in eight months.

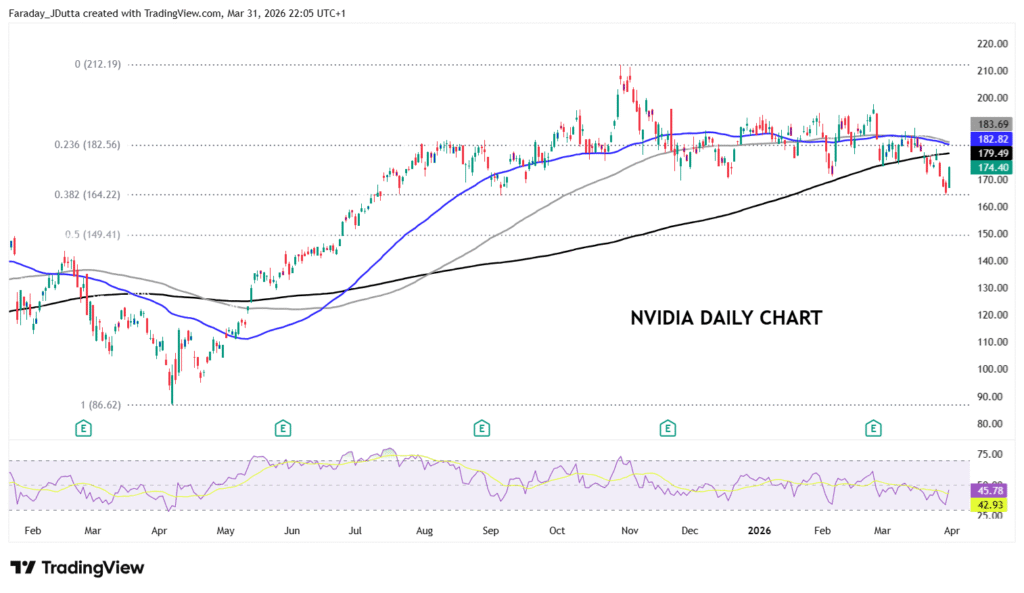

Chart of the Day – NVDA bounces off major Fib level

Semiconductor stocks climbed on the last day of the month and quarter as risk on sentiment boosted previously beaten-up tech stocks. Marvell Technology, which is set to receive a $2 billion investment from Nvidia, surged. Chart wise, prices actually tracked sideways after the onset of the Middle East war. But then tech selling took hold with NDVA falling below the 200-day SMA, now at $179.48. The stock slid to the major Fib retracement level (38.2%) of the Liberation Day low to record high at $164.22, a level last seen in September. The midpoint of that move sits below at $149.41. Bulls need to get back above the 200-day SMA and initial resistance zone which includes the 50- and 100-day SMAs and minor Fib level, all around $182.56.