Stocks hurt by ongoing geopolitical tensions, earnings mixed

Jamie Dutta >

Market Analyst

Jamie Dutta >

Market Analyst

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Wall Street ends lower with earnings weighing, revived trade tensions

* Gold extends Tuesday’s fall, Netflix plunges over 10%

* US sanctions Russia’s biggest oil producers, Rosneft and Lukoil

* Tesla profit tanks despite third quarter rush to buy EVs, stock off 1.7%

FX: USD was quiet and printed a doji more or less. Although there is lots going on in markets, there’s nothing to really drive as a big catalyst. The recent dollar upside is down to easing credit concerns, and a reversal of the debasement trade with the steep correction in gold. The dollar is susceptible to trade tensions between the US and China, while the CPI data on Friday looms.

EUR was marginally bid but generally quiet even as French lawmakers continue to negotiate the budget. The French-Germany 10-year spread is hovering around the lower end of its range since the August blow-up. The 100-day SMA is at 1.1654 and the 50-day SMA at 1.1688.

GBP slid to a low at 1.3305 before buyers stepped in. The soft inflation report was a surprise, with the headline below 4% at 3.8% and key services inflation also softer than expected. Rate cut expectations picked up, adding around 10bps by year end at one point after the data. The chances of a rate cut this year increased to above 70% before receding modestly.

JPY was the underperformer and retracing gains through the day. PM Takaichi is to tell President Trump that the country will buy US soybeans and LNG, though may not commit to a new defence spending target. Trump will visit Japan next week from October 27-29. On economic policy, Takaichi is reportedly readying an economic stimulus which is set to top nearly JPY 14tn. She also reaffirmed her support for the BoJ’s independence.

AUD continued to consolidate some more around 0.65 with little news flow. CAD strengthened with the major falling below 1.40 to near two-week lows. Stronger than expected Canadian CPI data for September lifted domestic yields and gave the loonie a break against the USD. But the risk of a BoC rate cut next week remains high.

US stocks: The S&P 500 lost 0.53% to close at 6,699. The Nasdaq moved lower by 0.99% to settle at 24,879. The Dow Jones finished at 46,591, down 0.71% on the day. Sectors were mixed with Industrials and Consumer Discretionary residing the laggards, while Energy outperformed, buoyed by gains in the crude. Texas Instrument and Netflix were the headline grabbers with weak forward next quarter guidance by the former. Netflix’s profits were hit by a Brazilian tax dispute but sales were in line and there looks to be continued positive subscriber and earnings momentum. Tesla reported record quarterly revenue after the US close, but earnings missed estimates and the stock sold off over 1%. Management emphasised an AI-led roadmap with Robotaxi pilots and new products like the Model 3 and Megapack 3/Megablock batteries.

Asian stocks: Futures are mixed. Stocks were muted after the mixed handover from Wall Street, amid earnings and the slump in precious metals. The ASX 200 fell back with major losses in mining stocks after gold fell the most in one day since 2013. The Nikkei 225 dropped below 49,000 though it made back some losses with focus on the new PM. The Hang Seng and Shanghai Comp were subdued with ongoing China-US trade tensions to the fore.

Gold dropped again though clawed back some losses through the US session. See below for more on bullion.

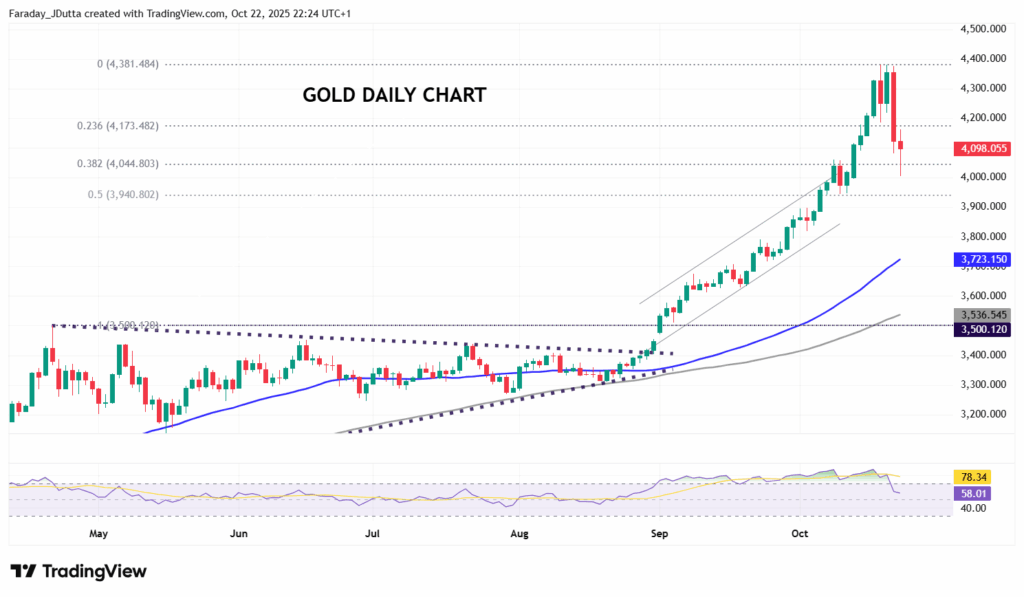

Chart of the Day – Profit taking sparks gold volatility

After suffering its worst single day in 12 years, and worst absolute fall on record, gold continued to remain volatile. Obviously, this comes after its stellar run with gains of 25% just in the last two months. The hugely overbought market was ripe for some profit taking with prices having gained as much as $1,000 since late August. The move higher in recent months has been mainly driven by ETF buying. Investors bought a record volume of gold ETFs last month, while the buying seen over the last month was the largest in terms of tonnage since March 2022. Central banks have continued to support bullion and inflation concerns are still present, while geopolitical tensions and dollar weakness are less compelling though hardly resolved. Prices dipped below a major Fib level (38.2%) of the September to October rally at $4,044. There’s a minor retracement level at $4,173 while the midpoint of that move sits at $3,940.