Nvidia beats and raises outlook boosting stock futures

Jamie Dutta >

Market Analyst

Jamie Dutta >

Market Analyst

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Equities advance around fading AI disruption fears

* AUD outperforms on hot inflation data and another rate hike in May

* Nvidia posts first $200bn year on back of AI investment boom

* HSBC surges to record on profit beat, raised targets; boosts FTSE 100

FX: USD again touched the 50-day SMA at 97.93 before closing lower with the market’s focus on NVDA and equity markets. President Trump’s annual State of the Union speech had little market impact as he touched upon many of last year’s key policy issues and was light on actual forward-looking signals. He emphasised that US will never allow Iran to gain a nuclear weapon, but said he wants ‘to solve the issue with diplomacy’, while he added that tariffs would remain in place. Brent crude is consolidating just below recent highs around $72.

EUR traded above the 50-day SMA at 1.1773 with sentiment still the big driver. Final euro area inflation data stayed unchanged with countrywide figures released on Friday. Markets continue to price a neutral path for rates with no moves for the foreseeable future.

GBP was the second strongest major as it traded above the 50-day SMA at 1.3531. Comments from the BoE’s Bailey continue to impact due to the less dovish tilt with worries about inflation expectations currently deemed important. April is still priced for a 25bps rate cut. Prices in cable are at the downward trendline from the recent January top.

JPY underperformed mildly as prices in the major pulled back from its intraday top at 156.82. The 50-day SMA sits at 155.95. Markets reacted to PM Takaichi’s latest nominees to the BoJ by pushing up long-term government bond yields as the picks are seen as doves and reflationists.

AUD outperformed on firmer than expected CPI data. The key measure of underlying inflation for the RBA, the trimmed mean, accelerated from 0.2% m/m to 0.3% and from 3.3% y/y to 3.4%. The numbers bolstered bets that the central bank could follow up on its inaugural 25 bps rate hike from earlier this month by the time of the May policy meeting, with a 92% chance of a second move.

US stocks: The S&P 500 gained 0.81% at 6,946, the Nasdaq was 1.41% higher at 25,329 and the Dow Jones settled higher by 0.63% at 49,482. Sectors were mixed with five in the green and six in the red. Tech, Financials and Communication Services led the gainers while defensive Industrials, Real Estate and Consumer Staples were the laggards. White House Official says Amazon, Google, and Oracle are to sign data centre agreements, Fox News reports. All eyes were on Nvidia who reported after the US close. The chipmaking giant smashed estimates with record revenue of $68.13bn vs $65.91bn expected and EPS of $1.62 beating the estimate of $1.53. It also offered blowout guidance with a midpoint of $78bn being $5bn more than forecast. CEO Huang also said its got enough supply on hand to meet demand, which is growing exponentially and enterprise adoption of agents is skyrocketing. The stock was up 2.5% after hours, with shares of Broadcom, TSMC and Micron all higher.

Asian stocks: Futures are green. APAC stocks traded higher on the Wall Street rebound. The ASX 200 enjoyed strong advances in tech and mining with little impact from hot inflation. The Nikkei 225 rallied to a fresh record high as yen weakness helped exporters. The Hang Seng and Shanghai Comp were also helped by the regional upbeat mood with some focus on the annual Hong Kong budget.

Gold made back most of the Tuesday losses as prices consolidated below this week’s high at $5,249 before giving up some of these gains later on. Silver rallied over 4% to new local highs since early February, clearing $90.

Day Ahead – UK By-Election

There’s a crunch Gorton and Denton by-election in the UK today. This fight for an MP seat is due to the prior officials resigning due to ill health. Polls suggest it’s a tight three-way race between the Greens, Reform and Labour. The worry for the government is a surge in support for the Green party, which is hiving off previous Labour supporters. This a traditional safe Labour seat so a big loss for the government could reignite doubts about PM Starmer’s leadership. Any replacement of the current regime would be from the left, implying more spending and potentially unwinding all the fiscal repairs carried out at the last Budget. This presents potential risk to gilts and GBP, though so far Starmer has been adept at fending off attempts to dislodge him.

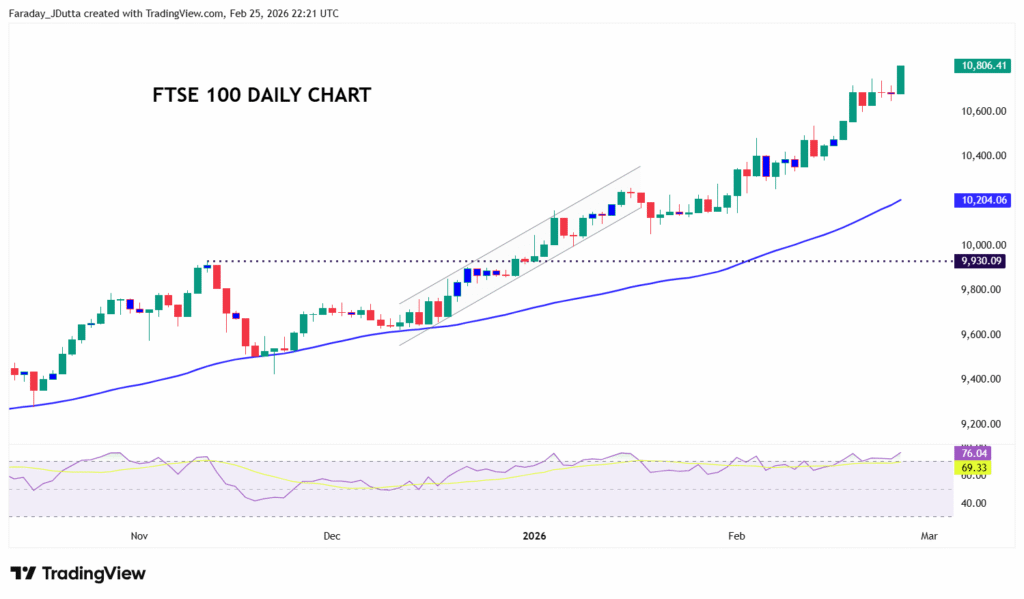

Chart of the Day – FTSE 100 continues to power ahead

The UK’s FTSE 100 continues to outperform other major indices. It’s up over 8.8% in 2026, versus a marginally positive S&P500. UK stocks still trade on lower valuation multiples and higher dividend yields than many US peers, anchoring steady returns. Of course, the sector mix is currently a big advantage as the index has a heavy weighting in energy, commodities, finance and defensives, all sectors which are rallying globally. The FTSE 100’s composition is a boon during rotations away from tech-centric leadership. The rate outlook and incoming inflation relief have also kept prospects of BoE rate cuts solid, with easing inflation trends buoying confidence in UK equities relative to US markets.