AI disruption fears and tariff chaos hurt sentiment

Jamie Dutta >

Market Analyst

Jamie Dutta >

Market Analyst

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Sour mood hits stocks, weighed by software and financials

* Gold jumps as risk-off concerns boost havens, JPY outperforms

* Trump warns higher tariffs for nations that ‘play games’ on deals

* IBM stock tumbles after Anthropic launches COBOL AI tool

FX: USD was relatively muted with competing drivers, which we wrote about in the Week Ahead. Tariffs are expected to come in a different form but with the same economic impact and a messy transition along the way. A mild “Sell America” theme kicked off again with White House (trade) policy uncertainty high again. The dollar has acted as a safe haven when oil markets have been involved, but otherwise has lost that dynamic. Iran tensions remain high even with a scheduled meeting for Thursday between the two sides.

EUR remained just above the 50-day SMA at 1.1772. Sentiment is the big driver with a more hard-nosed EU ready to negotiate new tariffs. The zone will likely not get any worse a trade deal than it already has, and one that European exporters have learnt to live with. This comes at a time when eurozone business sentiment continues to edge higher, after Friday’s PMIs signalled better growth, with Germany in the ascendancy and taking over from a stagnating France.

GBP tapped the 50-day SMA at 1.3527 but pulled back. Cable bounced off the 200-day SMA last week, which now sits at 1.3442, and the midpoint of the November to January move at 1.3429. We got dovish comments from MPC member Taylor, who was part of the 4-strong minority to vote for a rate cut earlier this month. He said the risk to the BoE forecasts were shifting towards lower inflation and higher damage to the economy from unemployment.

JPY outperformed on a safe haven bid though it faded the initial knee-jerk gains after the Asian session open. Prices hit the 100-day SMA at 154.89 and have just about remained below there. Sentiment and broader trade are the key current drivers.

US stocks: The S&P 500 lost 1.04% at 6,838, the Nasdaq was 1.21% lower at 24,709 and the Dow Jones settled lower by 1.66% at 48,804. Five sectors closed positive with one flat and five in the red, with Financials the worst performer. Fears of further AI disruption continued, while US President Trump hiked tariffs which sparked more policy uncertainty worries. A research piece by an independent house explored severe downside risks if AI exceeds expectations and emphasised how unemployment could spike to 10% with a recession in 2027. It highlighted payments, software and private credit stocks as highly exposed to such a scenario which all dropped on Monday. IBM plunged 13% as Anthropic announced that Claude can now automate COBOL modernisation efforts. Novo Nordisk dived more than 16% and wiped out its Wegovy-era gains on trial setbacks versus Eli Lilly’s weight loss drug, which boosted the latter by 4.9%.

Asian stocks: Futures are mixed. APAC stocks traded mixed on the US Supreme Court decision and mixed flat-rate tariff levels (10% to 15%) from President Trump over the weekend. The ASX 200 was dragged lower by tech, healthcare and real estate softness amid earnings releases. The 15% tariff rate is above the previously agreed 10%. The Hang Seng rallied as tech dominated. Japan and mainland China were closed.

Gold broke $5,200 as it pushed to a 3-week high and a 4-day win streak. Haven demand boosted bugs with policy uncertainty and the debasement underpinning support.

Day Ahead – State of the Union Speech

President Trump’s State of the Union will be in focus and no doubt grab all the headlines, though how market moving it will be is debatable. Consensus sees three themes around a strong economy, “America First 2.0” and projecting strength abroad. There may be talks about affordability too regarding everyday grocery, energy and drug prices ahead of the midterms.

Certainly, any hints on a new tariff framework after the Supreme Court ruling around the scope, sectors and timelines will be watched. More aggressive new levies would likely see higher Treasury yields and more risk-off, while more predictable tariffs see mild dollar selling. Rhetoric on Iran and broader geopolitical flashpoints could spill over into oil and risk sentiment. Gold as a hedge while legal fights, tariffs and Iran are hot keeps bullion bid.

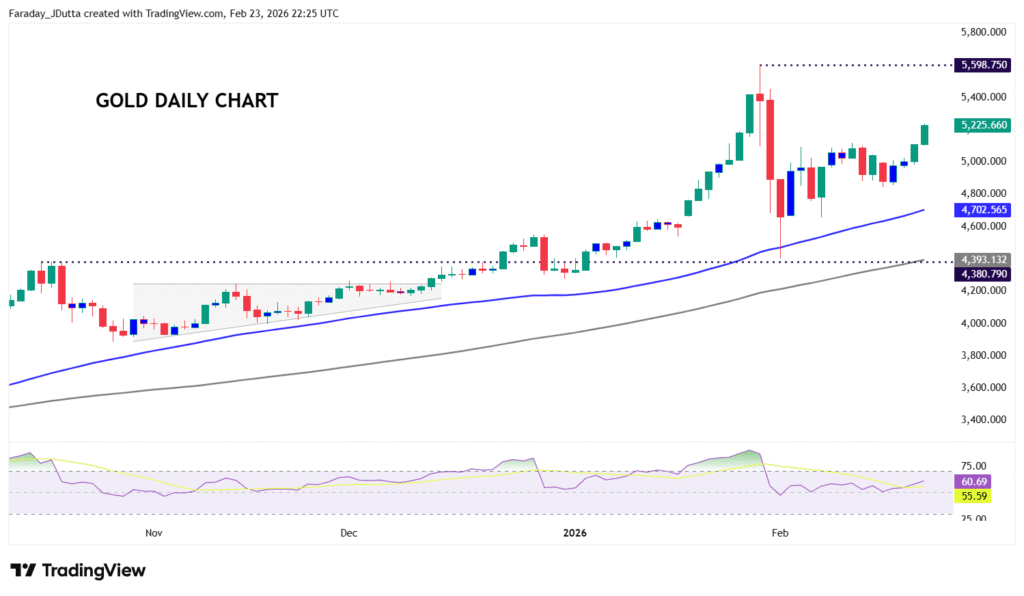

Chart of the Day – Gold heads north

After the torrid start to Febraury, after one of the biggest intraday sell-off in years, gold has steadied and the long-term underpinning of support remains. Prices spiked below the 50-day SMA around $4,472 on the first day of the month, but this indciator has proved strong support for many months, which is unsurpsiing since the long-term bull trend kicked off in October 2022. Recent volatility and then consolidation around $4,800 has seen prices recently move higher with a recent decisive psuh above $5,000. Central bank buying remains are key driver, along with Fed rate cut expectations and the debasement theme. Worres about fiscal deficits are attracting investors to heard assets. The record spike high sits at $5,598.