Crude falls as stocks gain on end of conflict hopes

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Iran currently reviewing new US proposal, yet to respond to new US text

* President Trump says Iran negotiations in final stages

* US stocks slide under pressure from higher interest rates, Fed minutes have hawkish bias

* Nvidia flat after revenue and guidance beat but steady margins show increased competiton

FX: USD turned lower after initially printing fresh cycle highs at 99.47 but closed off its lows. The 50-day SMA is still acting as support at 98.99. Dollar gains have been helped recently by higher Treasury yields. Indeed, the 10-year printed a fresh cycle high at 4.68%, a level last seen in January 2025, while the 30-year hit 5.12%, which was last seen in July 2007. However, the former printed a bearish candle and rejection of higher yields. Crude oil prices dropped quite sharply off 5% on hopes Iran will make a deal soon as President Trump said negotiations were in the final stages. The FOMC minutes confirmed a deeply divided Fed with a hawkish bias as the ‘majority’ saw a hike likely warranted and ‘many’ preferred removing the easing bias.

EUR rose versus the dollar but underperformed its major peers. Positioning by big funds and speculators is now far more balanced, suggesting that the risk of abrupt technical sell-offs is more contained. But the macro environment has clearly turned less supportive for the euro with eyes on today’s PMI figures.

GBP outperformed most of its peers again, as cable traded around the 50 and 200-day SMAs at 1.3422/26. April CPI data came in a touch softer than expected with the headline printing a fresh one-year low at 2.8% and the core extending its post-covid decline to 2.5%, a level last seen in 2021. BoE rate expectations have softened with only a 10% chance of a rate hike next month.

JPY lagged its peers but at least halted the run of seven consecutive days of losses. Prices have paused and consolidated around the 2025 top and 50-day SMA around 158.87/76. Recent MoF communication has been forceful with BoJ guidance continuing to lean hawkish.

US stocks: The S&P 500 added 1.08% to close at 7,433, the Nasdaq closed up 1.66% at 29,298 and the Dow Jones settled higher by 1.31% at 50,014. Stocks were positive on optimism over the Middle East conflict. Sector performance saw eight sectors in the green, with Consumer Discretionary and Tech leading the gainers. Energy was the big laggard as crude prices dropped over 5%. Semiconductors and memory names rallied ahead of Nvidia’s earnings. Nvidia reported after the bell and underwhelmed even as it beat on revenue and guidance. EPS hit $1.87 vs $1.76 and revenue was $81.62bn vs $78.86bn, while forward guidance was predicted at $91bn which was above estimates. But gross margins ‘only’ came in at 75%, meeting analysts’ expectations amid growing AI chip competition. The stock is marginally lower after hours. Retail stocks TJX and Target had mixed performances after their earnings with the former jumping 5.7% as it beat on top and bottom lines, but TGT slid 3.9% as it sounded cautious even though it reported its strongest sales gain in years.

Asian Stocks: Futures are mixed. APAC stocks fell following the weak lead from Wall Street, as inflation worries saw bond yields continue to rise. The ASX 200 retreated with mining and materials the main underperformers. The Nikkei 225 slid below 60,000 with comments on FX stoking intervention risks. The Shanghai Composite and Hang Seng were muted with mining and property stocks lower in the latter.

Gold found a bid and support at the minor Fib level of this year’s high-to low move at $4,452. Lower Treasury yields and dollar helped bugs.

Day Ahead – Australia Jobs, PMIs

Consensus expects 17.5k jobs to be added in April to the Australian economy, similar to the prior print, though the easter holidays may impact – ‘abnormal seasonality in a typical April has the capacity to surprise and over emphasise weakness. The unemployment rate is seen steady at 4.3%, with the fall at the start of the year proving temporary. Overall, the labour market has been in decent shape as policymakers watch in intently. The recent RBA May meeting noted that the board judged financial conditions would be somewhat restrictive after the May hike. Strong data with the headline above 30k and the jobless rate lower would push the odds a June rate hike of 11% higher. September sees a other 25bps move fully priced.

Eurozone data is likely to point to weaker momentum in the economy at the start of the second quarter, which comes after multi-month lows in the Composite and Services figures in April. The dilemma faced by the ECB is that the energy shock is hurting growth but pushing inflation higher. There’s above an 80% chance of a June rate hike currently priced in. The UK composite is expected to print just below the previous reading, as the prior front-loading boost from Iran war fears unwinds. Key will be input price inflation, which was the strongest since November 2022 in April. This week’s soft jobs and inflation data have dented rate hike bets with only a one in ten chance of a 25bps move in June which is not fully priced in until September.

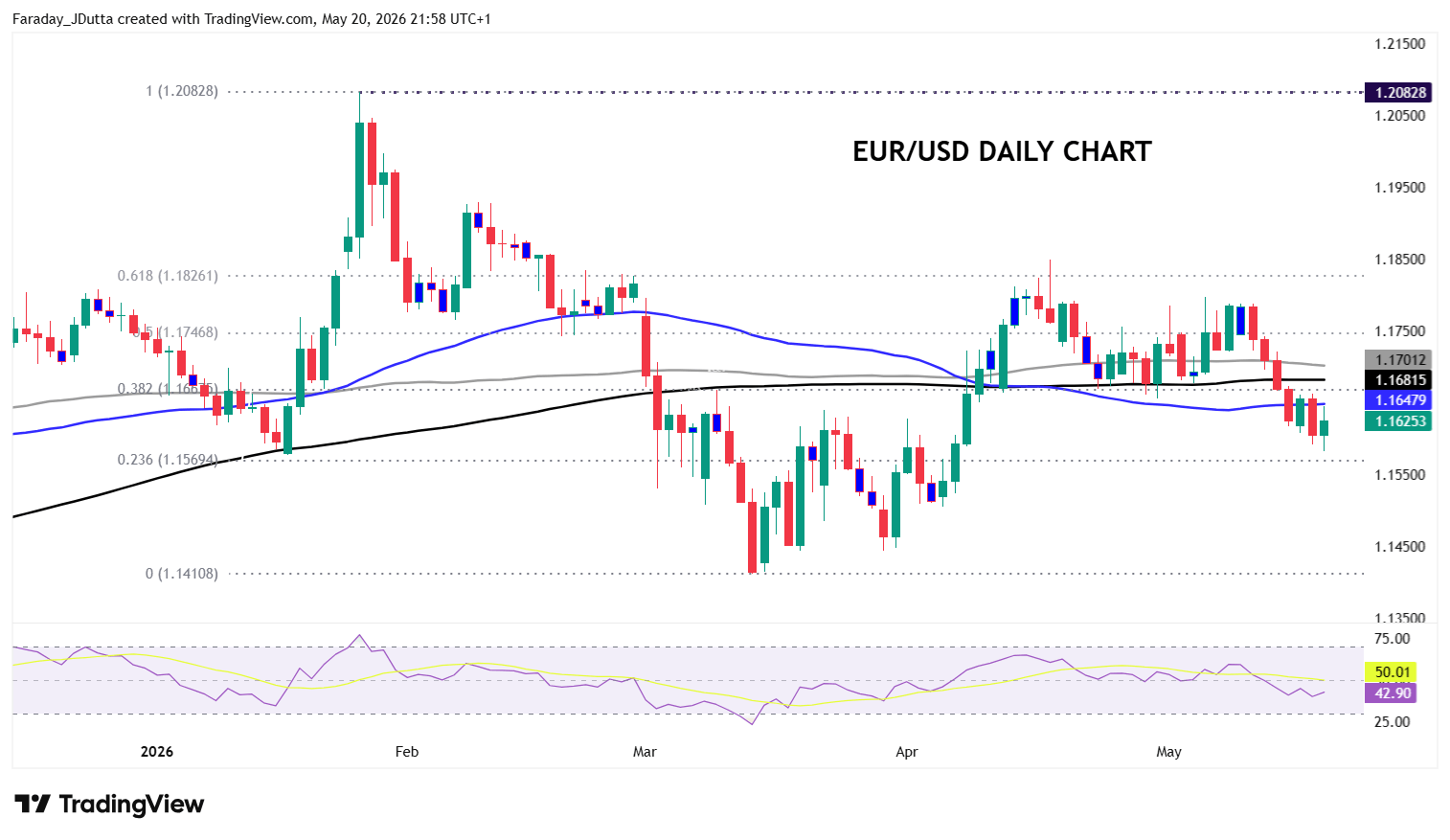

Chart of the Day – EUR/USD drifting lower

The world’s most traded currency pair looked to be breaking down after hitting 6-week lows. Positive Middle East headlines were thin, and the bar appeared to be getting higher for anything positive. Yet, ECB rate expectations are largely unchanged with more than three quarter point rate hikes price din by year-end, and policymakers are maintaining their cautiously hawkish guidance tying the rate outlook to the duration of the US/Iran conflict. A slither of optimism saw a bid yesterday, but broader momentum remains bearish with the RSI below 50. Bulls have stepped in for now and pushed the major back above 1.16. Near-term support is expected in the mid-1.15s, around the minor (23.6%) Fib retracement of the January-March pullback at 1.1569.